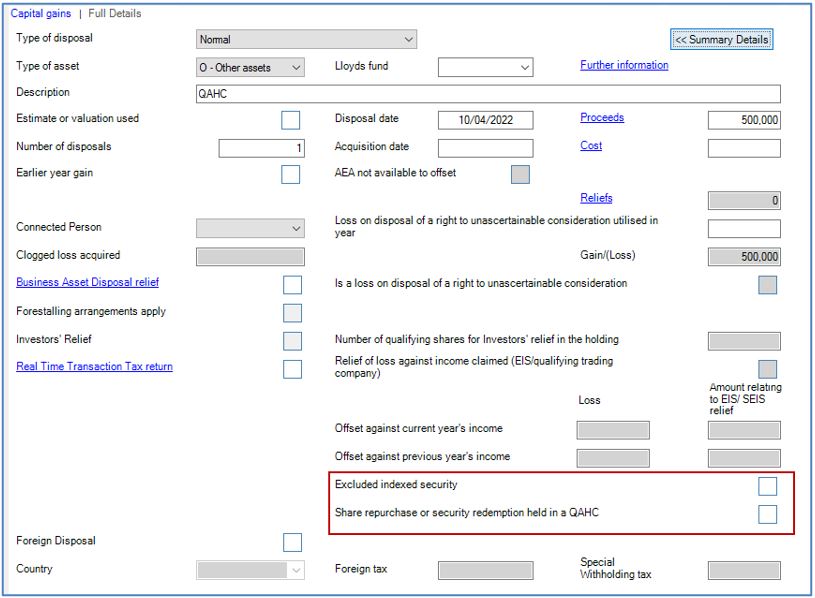

SA100 or SA900 – Qualifying Asset Holding Companies (251603 and 251598)

Gains on excluded indexed securities, and gains and losses on share repurchases and security redemptions from a qualifying asset holding company (QAHC) are reported as part of the total gains/losses for the year.

They are also required to be identified separately on the SA108 and SA905. This is for transactions on or after 6 April 2022.

Where the asset type is O, Q or U additional check boxes are enabled in the further details screen:

- Excluded Indexed Security

- Share repurchase or security redemption held in a QAHC

Note: HMRC have not made a change to the list of CGT reliefs published in the notes to SA108 and SA905 that can be used to reduce gains. It will be necessary to use one of the existing reliefs in order to reduce a gain made that is related to QAHC.